Granite quarterly update

Equity markets had one of their best quarters since Q2 2020, with AI remaining a key performance driver.

Chhad Aul, Chief Investment Officer and Head of Multi-Asset Solutions, SLGI Asset Management Inc.

What happened in the quarter?

Global markets started the first quarter (Q1) on stable footing. For the first couple of months of the year, equities continued to outperform bonds, but leadership within equities became more selective by focusing on sectors that are supported by the economy rather than spending. Excitement around AI faded, and investors’ focus shifted from broad spending to return on investment. This led to bigger differences in performance across technology-related sectors.

This shift supported a rotation away from the largest AI-driven U.S. technology companies and toward more cyclical and value-oriented areas of the market. International equities outperformed U.S. equities during the quarter. Canada, in particular stood out due to its attractive equity valuations and greater exposure to industries, like resources, which benefitted from a cyclical upswing.

Late in the quarter, the prevailing trend of equities outperforming bonds and international equities outperforming U.S. equities flipped as rising tensions between Iran and the United States became the single largest macro shock. This geopolitical escalation moved market attention toward supply risk and related concerns. The disruption to the Strait of Hormuz, which carries about one-fifth of global oil and liquefied natural gas flows, pushed oil prices sharply higher and raised the risk of renewed inflation and potentially more restrictive interest rate policy for central banks. Gold and the U.S. dollar initially benefitted from safe-haven demand though they moved unevenly as markets swung between escalation fears and hopes for a ceasefire.

Overall, Q1 started off with markets seeing a steady gain with divergence between winners and losers in AI-related stocks and continued strength in international stocks. However, that trend reversed with the U.S.-Iran geopolitical shock and energy related equities ending the quarter as the biggest winner.

| Top contributors/detractors | |

|---|---|

+ Tactical positioning: The Granite Funds’ tactical exposure to gold and oil was a significant contributor.1 Also contributing positively was a tactical underweight to international equities implemented in March due to rising geopolitical risk. The Granite Funds also benefited from a value-oriented defensive tilt in the U.S sector rotation sleeve.

- Manager selection in equities detracted from performance.

+ Strategic allocation: Canadian equities performed positively and contributed to return in the quarter. The commodities sleeve in Sun Life Real Assets Private Pool also contributed positively to return. |

|

What changes did we make?

In February, we selectively reduced exposure to S&P 500 equities as our indicators began to signal underlying weakness. Then in March, after the U.S.-Iran conflict began, we reduced our exposure to Europe, Australasia, and the Far East (EAFE) stocks as geopolitical tensions continued to build. We closed the above underweight at a profit towards quarter end and initiated an overweight to U.S. equities. During volatility, our systematic approach helped to identify a number of short-term opportunities that have shown an historical edge. Throughout the quarter, we also kept our overweight positions in gold and oil as inflationary hedges, which have been very positive contributors to returns.

Within U.S. equities, our proprietary sector rotation model guided the Granite Funds toward a more defensive stance, while maintaining exposure to inflation-sensitive sectors such as energy and materials. This positioning added meaningful value in Q1: technology and AI-related sectors came under pressure, while cyclical and value sectors held up better on a relative basis. Overall, these allocation decisions contributed positively to the Funds’ relative returns.

Recent notable manager and asset class changes (implemented Q4 2025)

Changes were also made to Sun Life Real Assets Private Pool,2 an underlying investment in the Granite Funds:

- Global REIT allocation increased from 35% → 50%

- Listed infrastructure increased from 35% → 40% for its stable income and defensive characteristics.

- Indirect exposure to commodities introduced at a 10% allocation for more direct inflation sensitivity and broader diversification.3

The strategic changes to add commodities to the portfolio as an asset class were timely as commodities were the best performing asset class in Q1 2026; the BMO Broad Commodity ETF gained nearly 26% in the first quarter.4

2Effective October 14, 2025, the Sun Life Real Assets Private Pool adopted changes to its investment strategies, Cohen & Steers Capital Management was appointed sub-advisor for the infrastructure portion of the fund, and SLGI Asset Management Inc., was appointed portfolio manager to manage the commodities portion of the Fund.

3Indirect exposure to commodities is achieved by investing in an underlying ETF that seeks to replicate the performance of the broad commodity market.

4NAV return as of March 31, 2026.

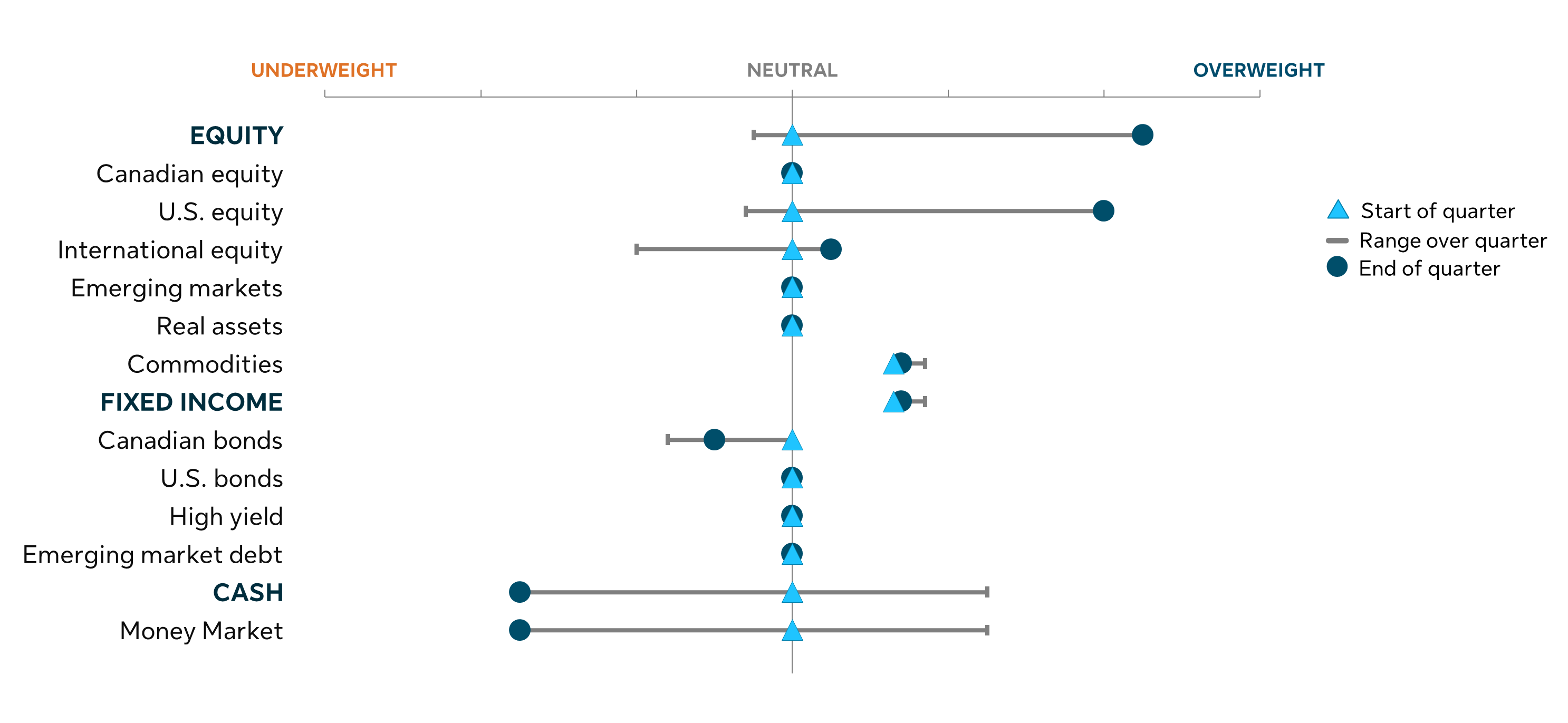

Q1 tactical asset class positioning

(Each line in the chart below shows the range of positions taken during the quarter. Circles represent beginning of quarter and triangles represents quarter end positioning)

What’s next?

Looking ahead, the most important driving force to the market will be the evolution of the U.S.-Iran conflict. With oil back above U.S. $100 a barrel5 and shipping through the Strait of Hormuz likely to continue being disrupted, the real risks are rising and sticky inflation. This may keep pressure on consumers and complicate the path for central banks.

On the bright side, AI is still a powerful growth driver, yet the story is starting to shift from excitement around buildout toward a more important question: which companies can turn spending into lasting profits? This likely means the next phase of the AI theme may be narrower, with leadership moving to firms that can show clearer monetization, solid earnings, and consistent cash-flow.

Looking ahead, the global economic growth and inflation outlook likely hinges on the outcome of the U.S.-Iran war. Diversification into inflation resistant assets such as real assets and commodities could play a very important role in the portfolio.

Based on our outlook, we enter Q2 2026 overweight in gold and oil as inflationary hedges, particularly against the backdrop of the ongoing U.S.–Iran conflict. At the same time, we have tactically added to equities in the near-term, as we believe upside potential on improving news flow is now greater than downside based on adverse headlines. While the conflict will likely remain a key market driver, the path toward resolution could create selective opportunities. In line with our systematic investment approach, we will continue to capitalize on short-term market dislocations as they arise.

5 As of March 31, 2026.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy. Mutual funds transact daily, and the metrics presented may change at any time, without notice. This commentary may contain forward-looking statements about the economy, and markets; their future performance, strategies or prospects. The words “may,” “could,” “should,” “would,” “suspect,” “outlook,” “believe,” “plan,” “anticipate,” “estimate,” “expect,” “intend,” “forecast,” “objective” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon. Forward-looking statements involve inherent risks and uncertainties about general economic factors, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. You are cautioned to not place undue reliance on these statements as a number of important factors could cause actual events or results to differ materially from those expressed or implied in any forward-looking statement. Before making any investment decisions, you are encouraged consider these and other factors carefully.