Q4 2025 | Market Update

Relative opportunities outside the U.S. widened over the quarter as monetary policy paths diverged and a weaker U.S. dollar helped non‑USD returns.

Highlights

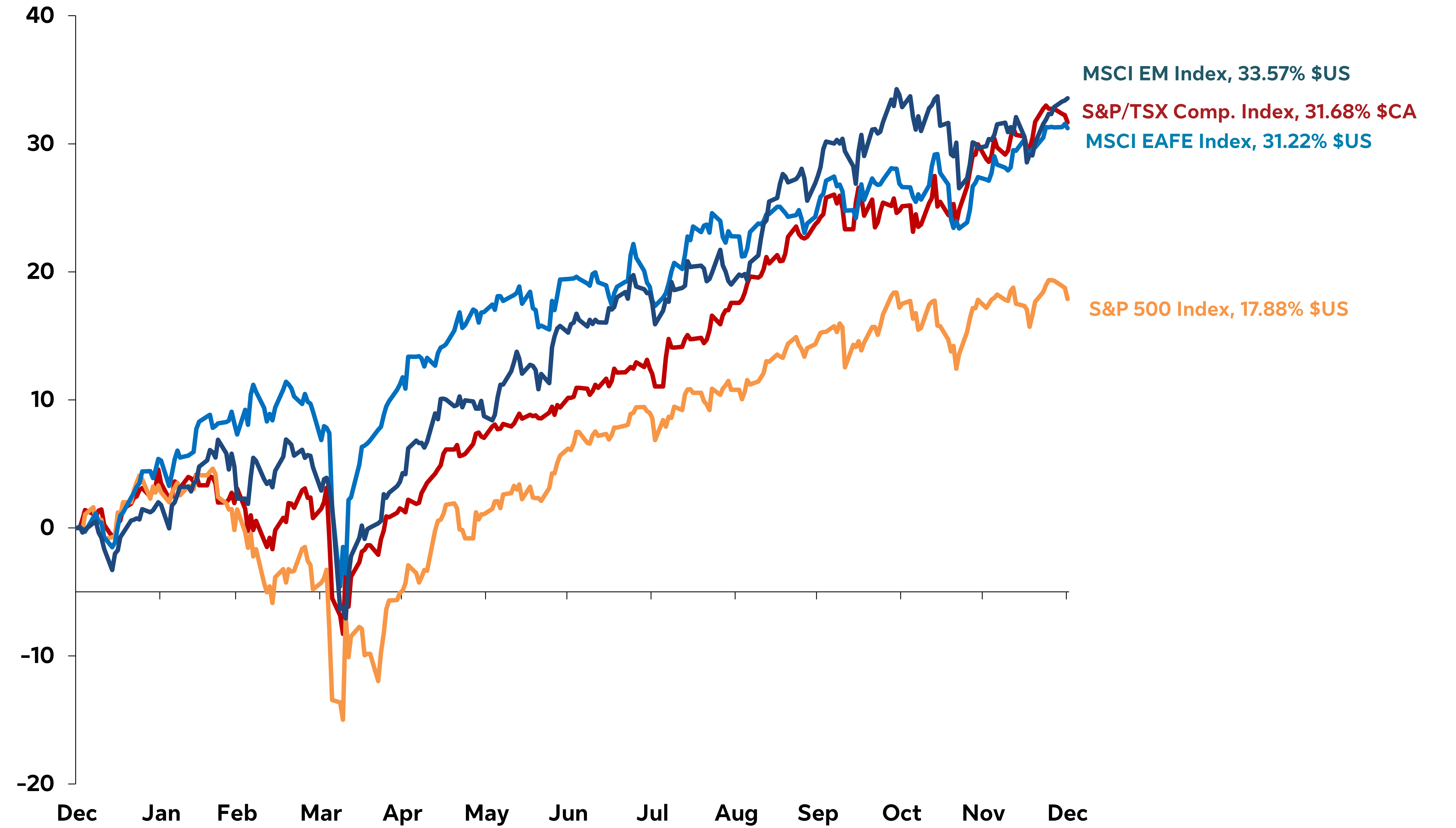

- Non‑U.S. equities outperformed the U.S. on greater market breadth, valuation normalization and a weaker U.S. dollar.

- Bonds posted modest gains, led by short and intermediate durations. Long-term bonds were more volatile based on their sensitivity to shifting rate-cut expectations.

- A continued weakening in the U.S. dollar could benefit non‑U.S. equities and commodities in the quarters ahead.

Equity markets continue to rise despite higher geopolitical tensions

Market performance was driven by central bank expectations, particularly the anticipated timing and pace of U.S. Federal Reserve (Fed) rate cuts in 2026. U.S. economic growth remained resilient, in contrast to slowing momentum in parts of Europe and China. Geopolitical tensions and tariffs added volatility but didn’t derail investors’ appetite for risk assets.

In Canada, the housing market, consumer sensitivity to interest rates and fiscal spending expectations helped shaped investor sentiment. Globally, rising AI capital expenditure remained a key theme, but scrutiny around returns on investment increased. Equity market leadership broadened outside the U.S., helped by a weaker U.S. dollar, while the U.S. market rally narrowed with a focus on AI.

By late 2025, several U.S. tariff announcements were walked back, but policy uncertainty persisted. A possible U.S. Supreme Court ruling in early 2026 could reverse International Emergency Economic Powers Act (IEEPA) tariffs, which could lead to longer-term uncertainty. Shorter term, however, a reversal of IEEPA tariffs could reignite inventory cycles and be positive for risk sentiment.

After cutting rates in October, the Bank of Canada (BoC) held its key interest rate steady in December. Markets largely believe the BoC is done lowering rates for this cycle. Conversely, the Fed is expected to continue to cut in 2026 as productivity and core inflation dynamics improve.

Non‑U.S. equities outperformed the U.S. on greater market breadth, valuation normalization and a weaker U.S. dollar. The S&P 500 Index gained 2.7%1 (USD) over the quarter, while the MSCI EAFE Index returned 4.9%1 (USD) and the MSCI Emerging Markets Index was up 4.8%1 (USD). Canadian equities performed well, with the S&P/TSX Composite Index gaining 6.3%.1 All returns are given on a total return basis.

Against this backdrop, we continue to diversify across regions, with an incremental emphasis on non-U.S. equities. Exposure to precious metals and real assets act as a portfolio hedge against policy and U.S. dollar uncertainty. Disciplined stock and manager selection remain key in emerging and international markets.

Graph 1: Non-U.S. equities outperformed

Total return, indexed to 0, as of December 31, 2024

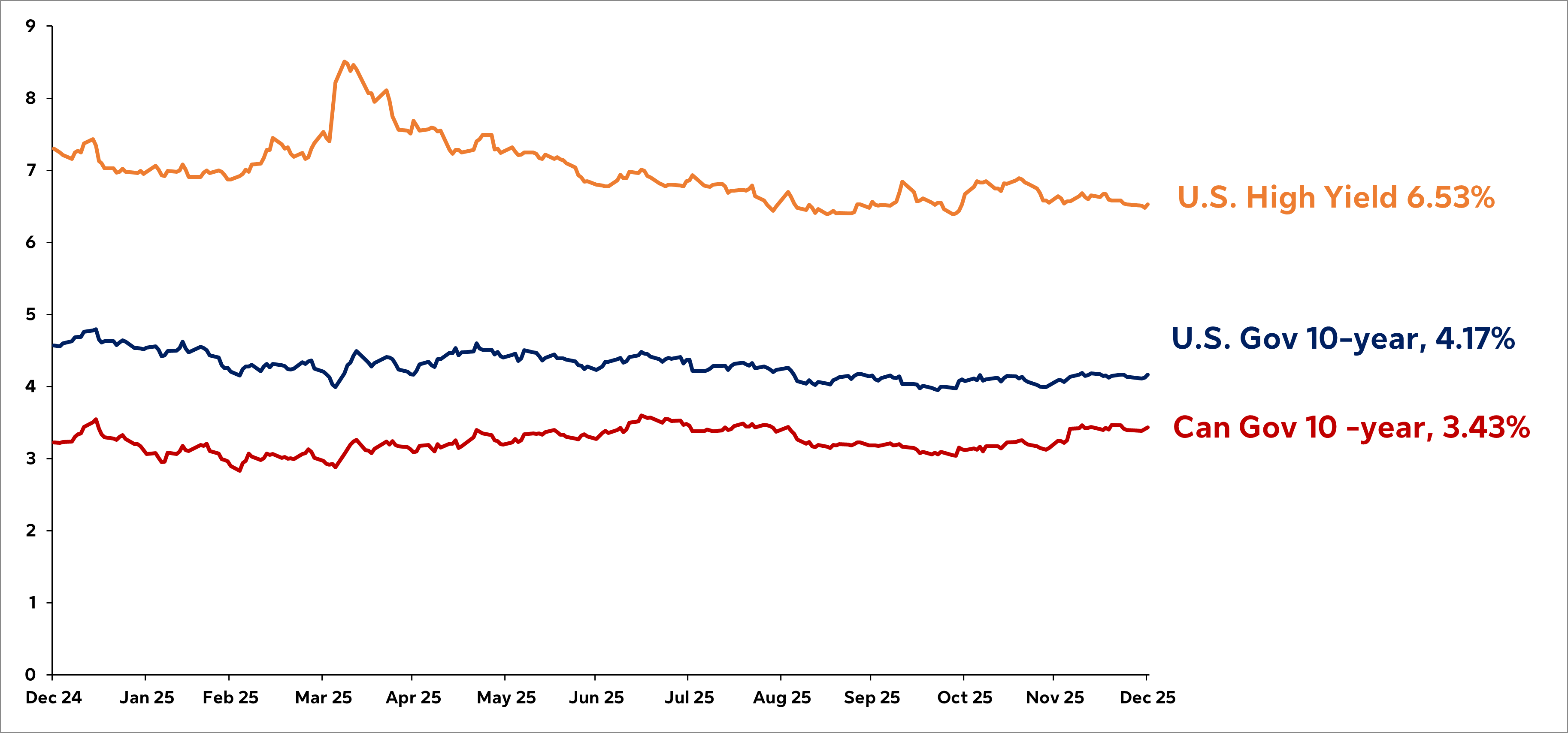

Bonds posted modest gains, led by short and intermediate durations, while long-term bonds were more volatile based on their sensitivity to shifting rate-cut expectations. Credit sectors were supported by stable growth and contained default risks. Investment grade (IG) credit benefited from stable spreads, while high yield (HY) was more idiosyncratic given narrow U.S. equity market leadership. In emerging market (EM) debt, divergent policy cycles led to greater variances among currencies and local interest rates.

Our Granite portfolios maintain a balanced duration stance and have selective EM bond exposure where real yields and policy credibility appear supportive.

Graph 2: Bonds see modest gains

U.S. and Canada bond yields

In the quarters ahead, Canadian inflation and wage growth are worth watching, specifically the pace of disinflation versus sticky components like shelter and food services. A mortgage renewal wave could have implications for consumer spending and loan performance, while we’re keeping an eye on corporate earnings for changes in consumer demand or any direct impact of fiscal spending.

In the U.S., jobless claims, layoffs and wage growth will be leading indicators of services inflation. A continued weakening in the U.S. dollar could be positive for non‑U.S. equities and commodities, but any reversal on trade policy would impact this. We’ll monitor corporate earnings for changes in consumer spending patterns, upward cost pressures, potential benefits of deregulation in sectors like financials, as well as capital investment and monetization opportunities from AI-related companies.

Key tactical changes

- Remained tactically overweight in gold: The price of gold, considered a safe-haven asset, continued to rise in Canadian-dollar terms, likely because of ongoing fiscal and monetary policy uncertainty, central bank buying and geopolitical tensions.

- U.S. sector rotation strategy: Selected sectors were tilted toward cyclical and value stocks, benefiting from a rotation away from the Magnificent 7.

1 Source: Bloomberg data as of December 31, 2025, all in total returns unless otherwise noted.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

This commentary may contain forward-looking statements about the economy and markets, their future performance, strategies or prospects or events and are subject to uncertainties that could cause actual results to differ materially from those expressed or implied in such statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon.