Challenges & Opportunities

In today’s market, headwinds in three areas will make it challenging to generate the strong returns we’ve seen in the last several years: rising inflation, low yields and high valuations. Christine Tan, Portfolio Manager, shares insights on these challenges, and how we are addressing them in our portfolios.

INFLATION | YIELDS | VALUATIONS

Rising inflation

The recent high inflation surprises appear to have been driven by transitory re-opening factors such as increased demand for used cars, a resumption of air travel, and a rise in the cost of restaurant food as consumers returned to in-restaurant dining. Continuing supply chain disruptions are another factor, with, for example, a strong surge in demand for semiconductors leading to a global shortage of chips needed in a broad range of products ranging from cars to video game consoles to computers. Although these supply disruptions will eventually normalize, it’s important to note that transitory inflation might stay elevated for longer than we think, because the world is not re-opening simultaneously, especially with the additional complication of new variants.

Low yields

Although interest rates are gradually increasing, we expect levels could remain low relative to history, which means lower cost of capital for investments and lower debt carrying costs for consumers and companies. We expect a gradual rise in yields from here as central banks appear to still be accommodative and view short term inflationary pressures as transitory. However, any indication otherwise, or an event like a poor Treasury auction, could trigger a sharp rise in yields and result in a risk asset sell off.

At the recent Jackson Hole symposium, Federal Reserve Chair Jay Powell reiterated the Fed’s dual mandate of maximum employment and price stability. He highlighted that while the pace of recovery has exceeded initial expectations with output surpassing prior peak in four quarters, the recovery in employment has lagged and been uneven. In-person service industries, which employ millions of workers, remain challenged both by inconsistent demand and worker shortage. While communicating that it might be time to commence a reduction of asset purchase program (quantitative easing or QE), he emphasized the taper would not necessarily signal or lead to a hike in interest rates. A change in interest rates would be subject to more stringent and substantive indications of sustained maximum employment similar to pre-pandemic levels.

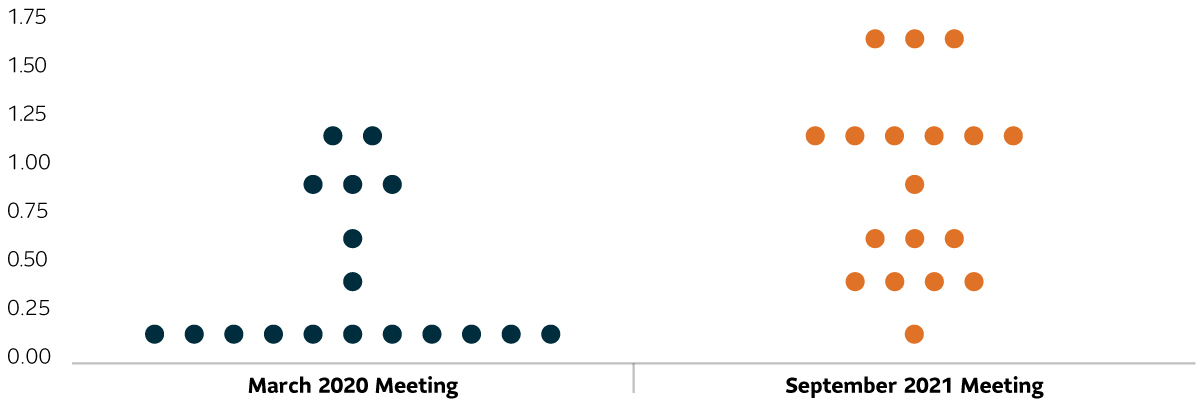

The Federal Open Market Committee (FOMC) dot plot (Chart 1) still shows a strong base expecting no rate hikes by year end 2023. However, movement up of several dots indicating a potential of up to two interest rate increases in 2023, versus a strong view in early 2020 that there would not be an increase until after 2023. The new Fed monetary policy regime is focused first on full employment and secondarily, targeting an average 2% inflation over the cycle. The change in language to “flexible average inflation target” (FAIT) provides the Fed with a lot of flexibility to respond to short term inflationary pressures.

Chart 1: Changing expectations on Fed policy rate

Source: Goldman Sachs

This shift in interest rate expectations have caused the spread between 10- and 30-year bond yields to narrow dramatically, which normally occurs when the Fed actually raises interest rates. Rates at the short end of the yield curve anticipated an increase in the key Fed rate, but longer duration yields fell in anticipation of a tightening Fed slowing the economy.

As a result of this change in rate hike expectations, the yield on benchmark U.S. 10-year Treasuries continued to surprise investors. After hitting 1.74% in March, yields retreated to around 1.32%. We believe yields will remain range bound but may slowly grind higher as we enter 2022.

For now, even though inflation indicators were running above the Fed’s target range, 10-year yields held to the 1.5% range before dipping lower in the first week of July and remains below 1.4%. This perhaps suggests that the bond market accepts Fed Chair Jerome Powell’s argument that inflation will be transitory and he will hold the line on interest rate increases. Or perhaps the bond market is telling us that economic growth will not be as strong as expected once we exit from the initial sharp post-lockdown recovery.

High valuations

The last downside risk is valuation. Both on the equity side, due to the strong performance from pandemic lows, but also on the fixed income side where yields remain relatively low while inflation expectations are increasing.

Value has outperformed growth since effective COVID-19 vaccines were first announced in November 2020, and we anticipate that trend will continue. However, we believe that the next phase of value performance may be focused on quality value. Companies with cyclical exposure, well-financed balance sheets, and a sustainable business model would benefit from the global economic reopening and recovery. Certain value sectors like financials, could benefit from higher yields and a steeper yield curve.

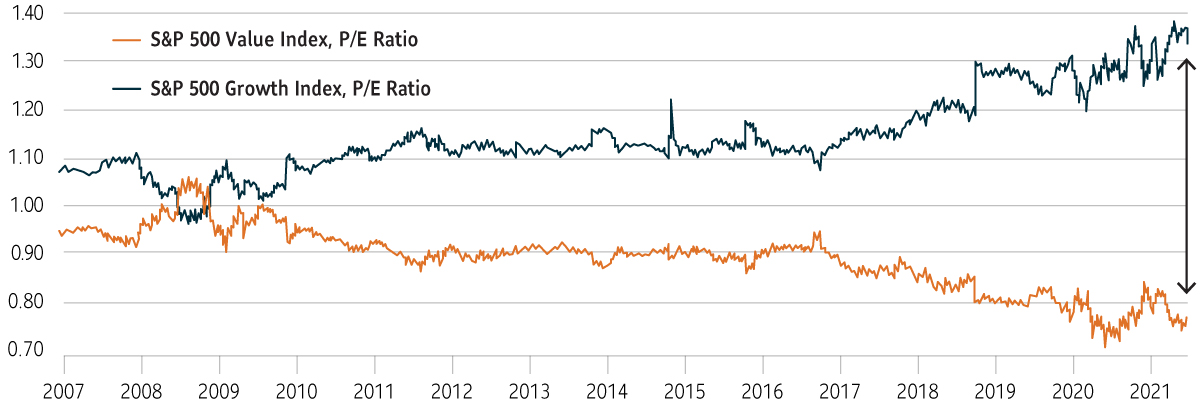

Despite the recent outperformance of value, the valuation gap between cyclical value and growth remains quite wide (Chart 2) so there could be more room for valuations to converge. We still like selective areas of growth, but also focus on quality and we are cautious in ensuring valuations are fair.

Chart 2: Valuation spread between growth and value still quite extreme

Source: Bloomberg. Data as of September 2021.

Solutions designed with multiple sources of return

Our target date fund and multi-strategy solutions are built on the firm belief that the strongest risk-adjusted returns are achieved through multiple sources—regardless of the current market environment. We accomplish this in four key ways:

- Open architecture

- Broader diversification

- Multi-manager approach

- Strategic blend of active & passive

The benefit of tactical asset allocation

And, because of our tactical asset allocation approach, we are able to adjust all of these sources to respond to the current environment. We actively monitor market conditions on an ongoing basis, and have the flexibility to respond to shorter-term risks and opportunities through tactical asset allocation. In other words, we can change the overall asset mix, underlying asset classes or styles (including active/passive) and add or remove managers to take advantage of potentially attractive opportunities from a risk-adjusted and capital preservation perspective.

To learn how we are positioning our funds in the current market environment, log in to download the full article: