Q2 2023 | Market Update

Markets rise spurred by high hopes for artificial intelligence and receding recession fears

Highlights

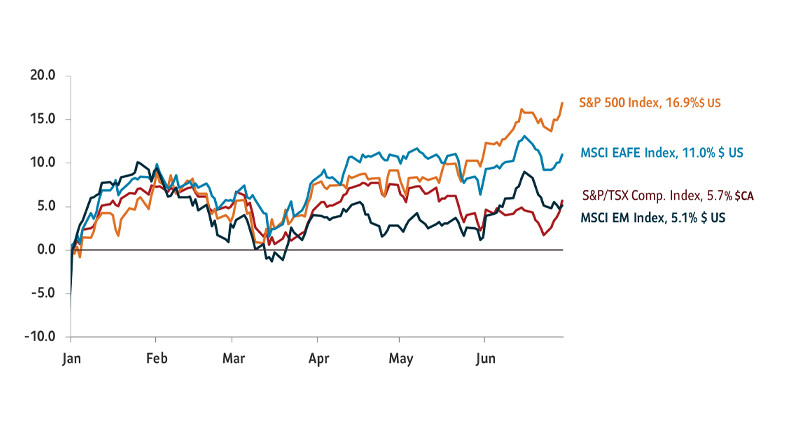

- U.S. equities rallied: The Nasdaq rose 32% and the S&P 500 rose 16% in the first half of 2023

- U.S. Consumer Price Inflation (CPI) rose 4% in May, the slowest pace since March 2021

- Canada’s CPI rose 3.4% in May, the weakest pace in two years

- Europe’s economic outlook weakened from high inflation and a slowing business outlook

- China’s economic rebound slowed on sluggish consumer spending, a debt-ridden property sector, and softening export growth

- Central banks across the developed world continued to emphasize the need for higher interest rates to bring down inflation to target levels

After falling most of last year, markets rose quickly in the first six months of 2023. Beginning in late 2022, markets sensed that inflation was receding and rose on expectations that central banks would cut interest rates by late 2023. Markets defied warnings from major central banks that interest rates would be higher for longer. This along with expectations about productivity gains from artificial intelligence fueled further rallies. In all, the tech-heavy Nasdaq had its best first-half calendar year performance since 1983. The S&P 500’s market capitalization jumped over USD$6 trillion.

Total return, indexed to 0 as of January 1, 2023

Source: Bloomberg. Data as of June 30, 2023.

We remain cautious about this recent rally in equities. Firstly, equity gains, driven by a handful of tech stocks, comes on the backdrop of tightening monetary policy. Our proprietary index made up of global central banks shows that monetary policy has become restrictive but global manufacturing that closely tracks this tightening, is yet to fall sharply. Secondly, our scenario of higher rates for the rest of 2023 is beginning to play out. Despite the downward trend in inflation, price growth remains above target. As of early July, central banks across North America, Europe and the U.K. reiterated their inflation-fighting stance with further interest rate hikes.

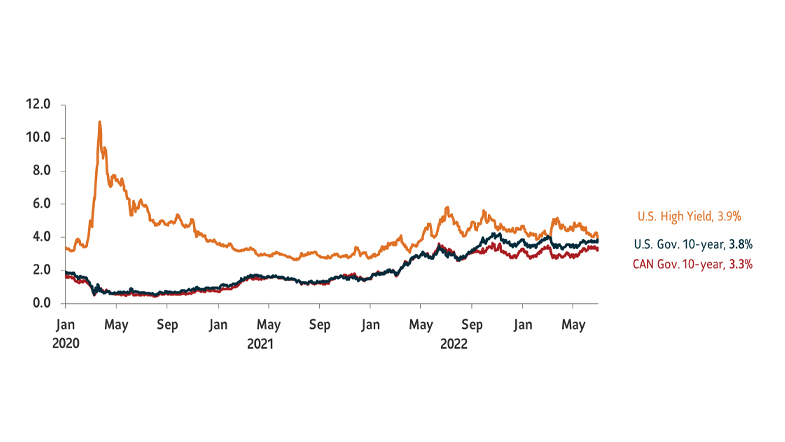

U.S. and Canada 10-year bond yields

Source: Macrobond. Data as of June 30, 2023.

The U.S. and Canadian economies have remained resilient so far and dodged expectations of a recession in mid-2023. But looking at labour market trends – rising unemployment claims and slowing hiring rates – we feel a slowdown has been delayed and not entirely avoided. We expect further challenges to the economy as pent-up consumer savings dwindle and consumers tighten their wallets. In Europe and China, economic growth is already facing headwinds.

Driven by sentiment and flows, the stellar first half for equities, has also left valuations stretched, especially in the U.S. technology sector. That is making us cautious about equities. On the other hand, we favour high quality fixed income. Despite a few rate hikes on the horizon, we estimate interest rates are closer to the peak. We see conditions turning favorable to high-quality bonds in case the economy cools.

Positioning

Equities: We remain underweight equities as key global central banks seem focused on beating inflation even if it harms the economy. Our underweight position in equities is spread across all geographies including Canadian, U.S., and global developed and emerging markets.

Fixed income: We favour bonds as we believe interest rates are close to peak levels. Within bonds, we favour Canadian investment grade bonds that can better withstand credit risks. In case the economy slows down or enters a recession, we see high-quality bonds adding diversification to portfolios. On the other hand, we are underweight risky credit and global high yield bonds, where yield spreads are tight and risk-adjusted return prospects remain less advantageous. We also remain neutral on cash.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund’s prospectus. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

This article contains information in summary form for your convenience, published SLGI Asset Management Inc. Although this article has been prepared from sources believed to be reliable, SLGI Asset Management Inc. cannot guarantee its accuracy or completeness and is intended to provide you with general information and should not be construed as providing specific individual financial, investment, tax, or legal advice. The views expressed are those of the author and not necessarily the opinions of SLGI Asset Management Inc. Please note, any future or forward looking statements contained in this article are speculative in nature and cannot be relied upon. There is no guarantee that these events will occur or in the manner speculated. Please speak with your professional advisors before acting on any information contained in this article.