Equities: De-risking portfolios to withstand growth risks

Across the developed world, rapid growth gave way to a perceptible slowdown in the second quarter of 2022. In the U.S., both consumers and businesses are showing increasing signs of fatigue. For instance, the ISM Manufacturing PMI, which started 2022 in the high 50’s, has now trickled to the low 50’s. The index measuring new orders in May fell nearly 6 points to 49.2, the largest drop since May 2020.

Further, consumer spending, which accounts for nearly two-thirds of the U.S. economy, advanced just 0.2% in May, the slowest pace of monthly gains this year according to data from the U.S. Department of Commerce. Additionally, U.S. consumer confidence, as measured by the Michigan Consumer Sentiment Index, hit a multi-decade low in June. With consumers strained, we believe U.S. corporations may face headwinds to pricing power and that profit margins for S&P 500 companies could slip from their current elevated levels.

The prospects for growth in developed markets outside the U.S., especially in Europe, look even more weak. Buffeted by an acute energy crisis, Germany, which accounts for about a third of the eurozone’s economic activity, grew just 0.7% in the first quarter of 2022. This was the slowest pace of growth for any country in the European Union other than Italy during this period. Other rate sensitive economies, such as Australia and Canada, are also heading for a growth slowdown as interest rate hikes work their way into the economy.

Given the bearish backdrop, we continued to increase the defensive positions within the Granite portfolios to navigate the volatile environment. During the second quarter, we took advantage of market rallies to de-risk our portfolios, positioning them for a slowing growth environment. We trimmed our overweight position in U.S. equities and stayed underweight in international developed equities. We also maintained our neutral positioning in emerging markets equities in the face of rising rates and a strengthening U.S. dollar.

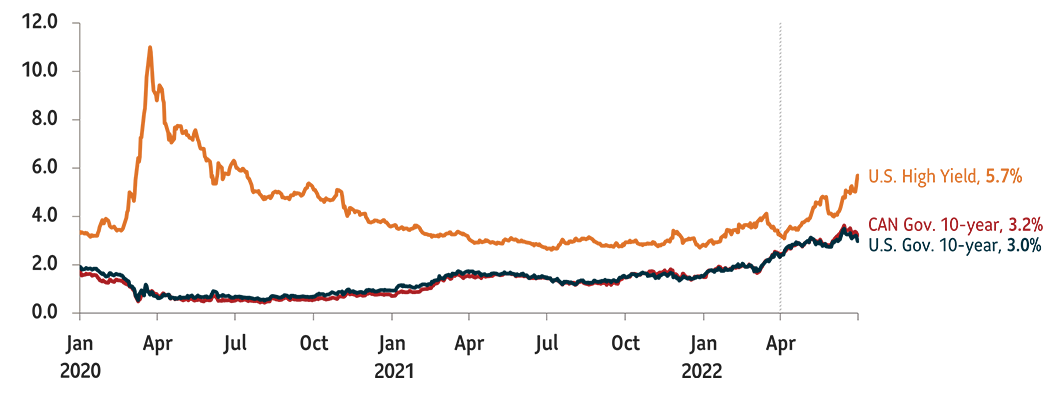

Fixed income: Underweight credit

As the Fed continued to raise short-term rates, bond markets suffered a historic rout during the June quarter. At its lowest point mid-June 2022, the Bloomberg U.S. Aggregate Bond Index returned -12% for the year, far exceeding its next worst performance of -2.9% recorded in 1984 and denting a three-decade bull market in bonds.

Further, the constant push and pull between inflation expectations and recession fears with an aggressive Fed in the background meant that 2-Year Treasuries continue to catch up with 10-Year Treasury notes. The spread between these two maturities ended the quarter flat indicating yet another sign of slowing growth in the U.S.

Frantic action in bond markets drove significant fixed income volatility. The MOVE gauge of volatility sprang to its highest level since March 2020, as bond market participants struggled for direction. Other bond market indicators such as rising spreads for junk bonds and the cost of protecting corporate bonds against defaults point to further difficulties.

We believe policy makers will be laser focussed on tightening until inflation data, which is lagging in nature, has shown a sustained cooling trend while paying less attention to softening economic leading indicators. Under this scenario of rising risks and elevated borrowing costs, we have grown cautious on credit. We have maintained our underweight to U.S. and emerging market investment grade bonds. Given our concerns on economic risks, we reduced our position in high yield bonds over the quarter. On the other hand, we continued to add to high quality bonds, more specifically to our core Canadian bond component as yields became more attractive. In addition, we also maintained our overweight position in cash to deal with any possible episodes of elevated volatility in the wake of aggressive central bank action.